What Happens If South Africa Runs Out of Fuel?

Not a panic piece. A clear-eyed look at how South Africa actually gets its fuel, where the system is genuinely vulnerable, how shortages develop in practice, and what the country’s safety nets look like — and where some of them have holes.

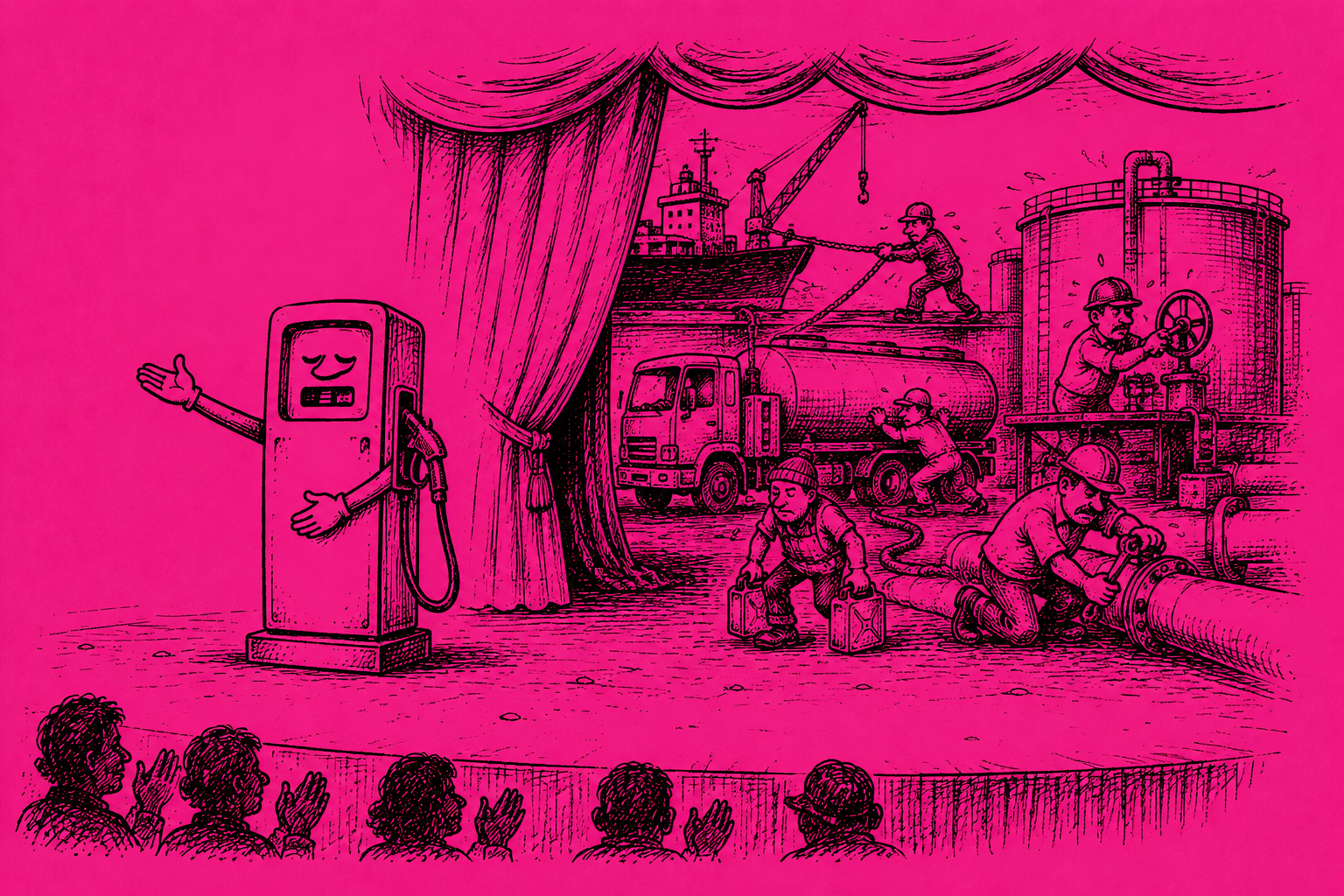

South Africa does not produce enough crude oil to fuel itself. It never has. The country’s entire liquid fuel supply — the diesel in every truck, the petrol in every car, the jet fuel in every aircraft — depends on a combination of imports, a refining base that has been contracting for years, a single critical port, a pipeline network that is aging, and a state-owned logistics company that has faced serious structural challenges. Understanding the system is not fearmongering. It is the precondition for understanding what risk actually looks like.

How South Africa Actually Gets Its Fuel

The supply picture is more precarious than most people assume.

South Africa’s domestic refining capacity has declined significantly. SAPREF — the Shell/BP joint venture in Durban and historically the country’s largest refinery — ceased operations. The Engen refinery in Durban has also closed. What remains is NATREF in Sasolburg (a Sasol/TotalEnergies joint venture), Sasol’s coal-to-liquids and gas-to-liquids plants in Secunda and Sasolburg (which produce diesel and petrol from coal and natural gas rather than crude oil), and the Astron Energy refinery in Cape Town, which has operated intermittently after significant investment challenges.

The gap between what domestic production covers and what the country consumes is made up by imports — refined product arriving by sea, primarily at Durban. This is not a marginal supplement. It is a structural, permanent dependency. South Africa imports crude oil for refining from the Middle East (Saudi Arabia, UAE, Kuwait, and Iraq feature significantly) and West Africa (Nigeria, Angola). It also imports substantial volumes of already-refined diesel and petrol directly, particularly as domestic refining capacity has shrunk.

Crude Oil Refining

Crude oil arrives by tanker, is refined into petroleum products, and enters the distribution system. With fewer operational refineries, this pillar is weaker today than it was a decade ago. Each refinery closure reduces the country’s ability to process crude into product domestically and increases the volume of finished product that must be sourced from international markets, which adds cost, complexity, and lead time.

Synthetic Fuels from Sasol

Sasol’s operations at Secunda and Sasolburg produce diesel, petrol, and other fuels from coal via the Fischer-Tropsch process, and from natural gas. This is a domestically produced buffer that is not dependent on crude oil imports or sea routes — a genuine energy security asset. However, Sasol’s production is not sufficient to cover the national shortfall alone, and Sasol’s operations carry their own input dependencies (coal supply, water, electricity).

Refined Product Imports

Finished diesel and petrol imported directly, primarily arriving at Durban harbour aboard product tankers. This is the most import-dependent component and the most exposed to international price movements, shipping disruptions, and foreign exchange fluctuations. A weakening rand increases the rand cost of every litre imported, even if the dollar price is unchanged. South Africa’s fuel price is denominated in a currency that is not the currency in which fuel is purchased internationally.

Strategic Reserves

Held by the Strategic Fuel Fund (SFF), a subsidiary of the Central Energy Fund (CEF). This is South Africa’s emergency buffer — crude oil and refined product stored specifically to cover supply disruptions. The SFF maintains storage at several sites, with the Saldanha Bay facility on the West Coast being among the most significant strategic crude storage locations in the country. The size, condition, and governance of this reserve matters enormously — and has not always been managed without controversy.

Strategic Reserves — The Buffer That Was Sold

South Africa has strategic reserves. It also has a cautionary story about what happens when they aren’t protected.

Under the Petroleum Products Act and associated regulations, South Africa maintains minimum stock obligations. Oil companies are required to hold minimum volumes of product in-country as a regulatory condition of operating. Above this commercial minimum, the state holds strategic reserves through the SFF — crude oil and refined product intended not for sale but for drawdown in a national supply emergency.

Strategic reserves exist because fuel supply chains are inherently international and subject to disruptions no single country controls: shipping delays, geopolitical events, refinery fires, natural disasters at supply origin points, or global price shocks that temporarily make procurement economically impossible. A strategic reserve buys time — typically measured in weeks of national consumption — for the supply chain to recover.

In 2015 and 2016, the SFF became the subject of one of the most damaging energy sector scandals in South Africa’s post-apartheid history. The then-CEO of the SFF, Sibusiso Gamede, authorised the sale of a significant portion of the country’s strategic crude oil reserves — reportedly around 10 million barrels stored at the Saldanha Bay facility — at what was described as below-market prices, without the required ministerial and board authorisation. The transactions generated hundreds of millions of rands. Where much of that money went became the subject of a Parliamentary inquiry, a Hawks investigation, and multiple legal proceedings that dragged on for years.

The consequence most relevant to energy security: the strategic reserve buffer that South Africa was supposed to have was substantially depleted. Rebuilding strategic reserves requires purchasing crude or refined product on international markets at market prices. Given the fiscal constraints the South African government has faced since 2016, how fully those reserves have been reconstituted remains a legitimate question for public accountability.

The Chokepoints

The system has specific vulnerabilities. They are geographic, infrastructural, and institutional.

A fuel supply system fails at its weakest link. South Africa’s supply chain has several links that are structurally difficult to route around.

Durban Port — The Single Import Gateway

The overwhelming majority of South Africa’s liquid fuel imports arrive through the Port of Durban. There is no equivalent backup at the scale required to substitute for it. Cape Town has import terminal infrastructure, but its capacity and the logistical distances involved make it a supplement, not a replacement, for Durban’s role in supplying Gauteng and the inland economic core. Anything that disrupts Durban port disrupts the national fuel supply. The July 2021 unrest demonstrated this vividly: several days of port disruption, combined with interruptions to the Transnet pipeline, produced forecourt queues across Gauteng within 72 hours and regional shortages in KwaZulu-Natal that lasted longer. The April 2022 flooding caused further port and pipeline damage that took weeks to fully clear. Neither event was a theoretical scenario — both happened within a 12-month window.

The Transnet Pipeline — Volume That Cannot Be Replaced by Road

The Transnet multi-product pipeline moves volumes that road transport simply cannot replicate. The pipeline carries millions of litres per day from Durban to the Gauteng terminal complex. To move an equivalent daily volume by road tanker would require thousands of tanker movements every single day — a figure that exceeds South Africa’s available tanker fleet capacity and would impose an impossible burden on the N3 highway. If the pipeline goes down for an extended period, Gauteng runs on terminal stock and the strategic reserve. Terminal stock is typically measured in days to weeks. After that, the pipeline’s absence becomes a genuine crisis.

Transnet Pipelines has faced the same infrastructure investment deficit that has affected Transnet’s ports and rail operations: deferred maintenance, aging pump station equipment, skills losses, and governance challenges documented extensively in the Zondo Commission findings. A pipeline that is not maintained is a pipeline that will eventually fail — not dramatically and suddenly, but progressively and at increasingly inconvenient moments.

Eskom Load Shedding — The Hidden Supply Chain Risk

This one rarely features in fuel security discussions, but it is real. Pipeline pump stations require electricity. Storage terminal operations — tank pumps, loading rack systems, metering equipment — require electricity. Port cranes and container handling equipment require electricity. Fuel dispensers at forecourts require electricity. Sustained Stage 6 load shedding doesn’t shut these systems down outright — most have diesel backup generators (the irony is noted) — but it adds operational friction across every stage of the supply chain simultaneously. It slows port turnaround. It reduces pipeline throughput. It increases the operational cost and complexity of maintaining supply. During extended high-stage load shedding, the supply chain tightens in ways that don’t make headlines but are visible to operators inside the system.

The Rand Exchange Rate — Procurement Risk

Crude oil and refined petroleum products are priced in US dollars on international markets. South Africa pays for them in rands converted to dollars. A rapid, sustained rand depreciation — of the kind the ZAR has periodically experienced during political crises or global risk-off events — raises the rand cost of every import without any change in the underlying global price. If the depreciation is severe enough and sustained enough, it creates procurement stress: oil companies and importers face a cost-versus-regulated-price tension, since South Africa’s pump prices are regulated and adjusted monthly rather than in real time. A severe rand move in a given month can make fuel imports uneconomical against the prevailing regulated price, creating incentives to delay procurement — which tightens available stock. This mechanism is subtle, entirely financial in nature, and produces real-world supply effects.

How Shortages Actually Develop

A nationwide fuel shortage doesn’t start with empty pumps. It starts weeks earlier, invisibly.

The public experience of a fuel shortage is queuing at a forecourt. The industry experience of a developing shortage starts much earlier, in stock level data, delivery docket reconciliations, and procurement lead times. By the time queues form at a pump, the shortage has been building in the system for days or weeks. Understanding that timeline matters for understanding both how the country is vulnerable and where interventions are possible.

The panic-buying amplification effect is one of the most predictable and damaging dynamics in any fuel supply disruption. A 10% supply shortfall, rationally managed, produces mild inconvenience. The same 10% shortfall, amplified by social media-driven panic buying that doubles demand overnight, produces visible queues and a crisis narrative that is almost impossible to walk back quickly. The psychology of fuel hoarding is, in practice, as significant a factor in shortage severity as the underlying supply gap.

What Would Actually Happen

Not a collapse. A cascade — with intervention points at each stage.

A complete, nationwide fuel outage — every pump in the country empty simultaneously — is not a realistic scenario. What is realistic, and has happened to varying degrees, is a severe, prolonged shortage concentrated in specific regions or specific products. Understanding the cascade of consequences from that scenario is more useful than imagining an apocalyptic total failure.

Essential Services Prioritised, Then Strained

Government would invoke disaster management powers and establish fuel allocation priorities: hospitals, emergency services, police, military, and water treatment facilities first. These allocations are planned on paper. In practice, executing them requires a functioning logistics network — trucks to move the allocated fuel, drivers to drive them, and a sufficiently intact supply chain to draw from. A severe shortage strains all of these simultaneously. Hospitals that have diesel generators need those generators to keep running. If their generator fuel runs low, load shedding and a fuel shortage coincide in a genuinely dangerous way for critical facilities.

Logistics and Food Supply

South Africa’s food distribution system is diesel-dependent at every stage: farm equipment, refrigerated trucks, distribution centre forklifts, delivery vehicles. A sustained diesel shortage — measured in weeks, not days — begins compressing food supply into urban centres within 5 to 7 days. Perishables are affected first. Staple goods follow. A country that is already food-insecure at the margin does not have large buffers between a logistics disruption and visible food access problems in lower-income areas.

Mining and Industrial Production

South Africa’s mining sector — platinum, gold, coal, chrome — is among the most diesel-intensive industries on the continent. Underground mining equipment, haul trucks, processing facilities, and the logistics chain that moves ore and product all run on diesel. A prolonged shortage halts production at mines, which has foreign exchange consequences (mining is a primary export earner), employment consequences, and downstream industrial consequences for electricity generation (coal) and manufacturing (raw materials). The economic damage compounds non-linearly the longer a shortage persists.

Government Response Mechanisms

South Africa does have response tools. The Minister of Mineral Resources and Energy has powers under the Petroleum Products Act to direct the allocation, price, and distribution of fuel under emergency conditions. Strategic reserves can be released. Import emergency procurement can be authorised outside normal procurement processes. Regional fuel rationing mechanisms can be activated. The question is not whether these tools exist — they do — but whether they can be deployed quickly enough, at sufficient scale, with sufficient institutional competence, given the governance challenges that have affected key entities in the supply chain. The tools are in the legislation. Their operational readiness is a separate matter.

The Honest Assessment

South Africa is not on the verge of running out of fuel. The supply chain has depth, the country has reserves, and there are multiple production inputs that don’t share all the same vulnerabilities. A total national outage is not the realistic risk.

The realistic risk is more specific: a significant disruption at Durban port, combined with a Transnet pipeline fault, sustained over two to three weeks, during a period of rand weakness, could produce genuine regional shortages severe enough to disrupt logistics, food supply, and industrial production in Gauteng and KwaZulu-Natal. All three of those conditions have individually materialised in recent years. Their simultaneous occurrence is not a far-fetched scenario.

The structural vulnerabilities — import dependency through a single port, an aging pipeline managed by a state entity with documented governance problems, strategic reserves whose reconstitution after the SFF scandal has not been fully accounted for publicly, and a refining base that has contracted — are real. They don’t make a crisis inevitable. They do mean the margin for error is narrower than it once was, and that the country has less capacity to absorb multiple simultaneous shocks than the system was originally designed to handle.

The most consequential thing a well-informed citizen can understand about fuel security is this: the early-warning signs of a developing shortage are visible weeks before queues form at pumps. The decisions that determine whether a disruption becomes a crisis are made in procurement offices, government departments, and logistics control rooms — not at the forecourt. By the time the public sees a problem, the window for easy intervention has usually already closed.